20 May 2026

Demystifying Merchant Account Verifications That Shield Recurring Credit Card Flows From Unauthorized Activity

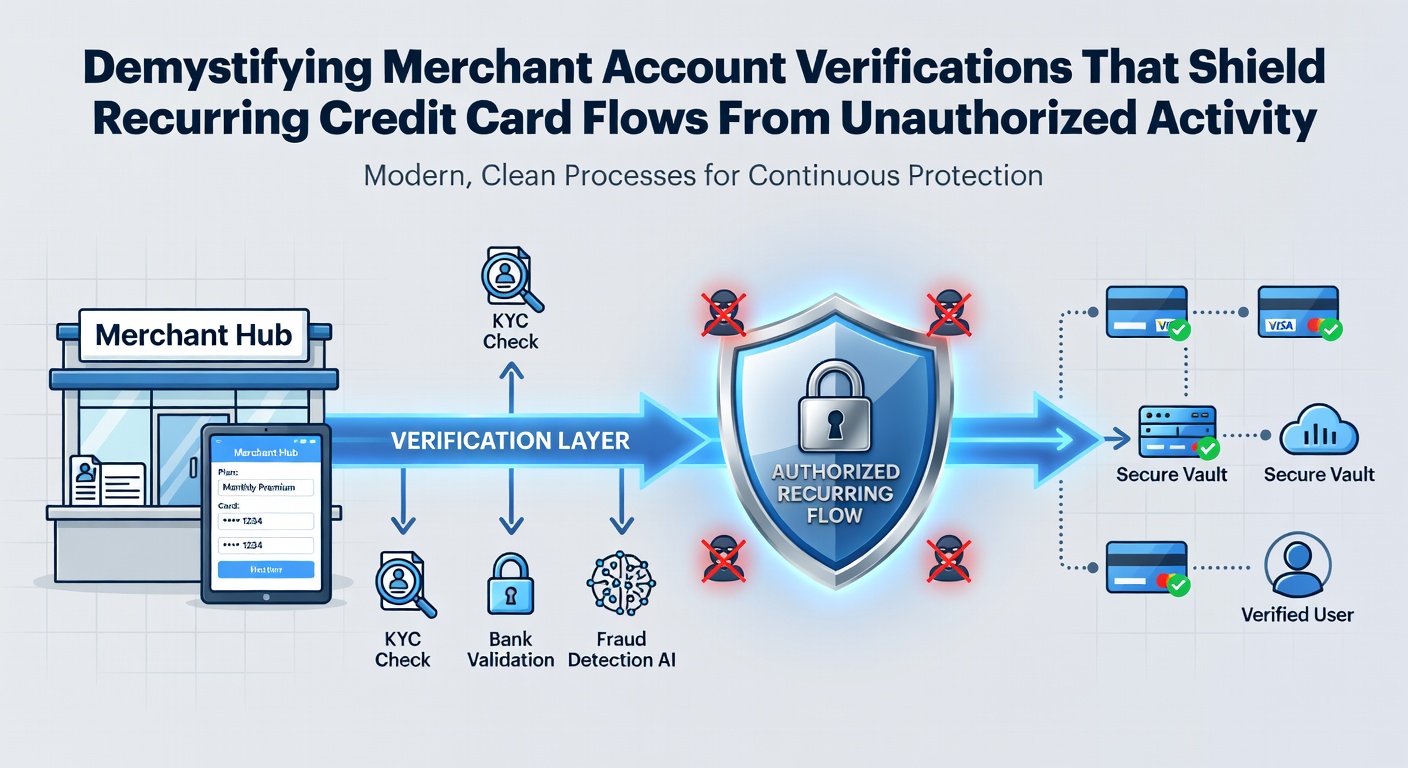

Merchant account verifications serve as foundational checks that confirm business legitimacy and transaction integrity before recurring credit card payments begin processing. These procedures examine details such as business registration, bank account linkage, and ownership documentation, while they establish secure pathways for ongoing billing cycles that protect against unauthorized charges. Research from the Federal Reserve indicates that structured verification steps reduce initial fraud exposure in subscription-based models by establishing clear authorization trails from the outset.

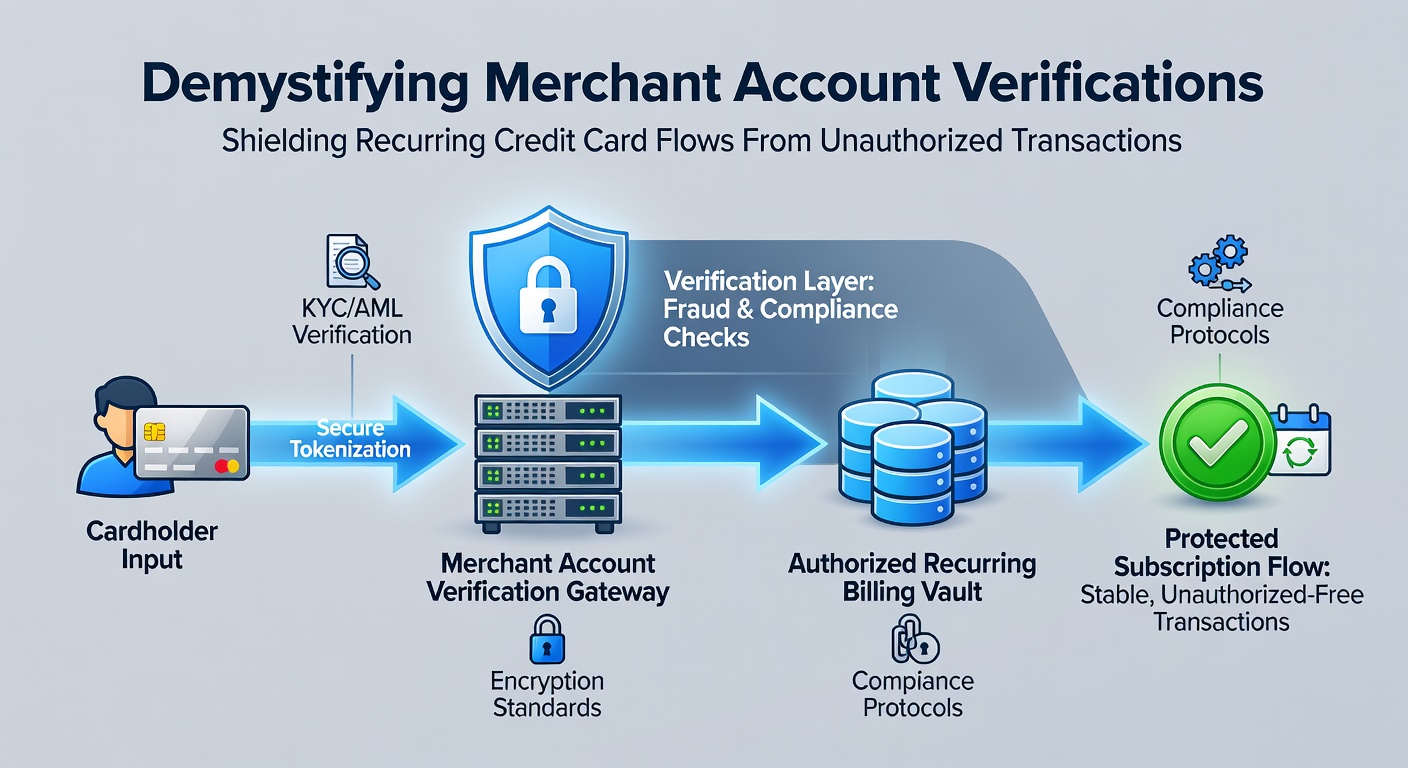

Recurring payment flows introduce unique vulnerabilities because card details remain stored and charged repeatedly without fresh customer interaction each time. Observers note that verifications address this by requiring merchants to demonstrate compliance with standards like those outlined by the PCI Security Standards Council, which mandate tokenization and encrypted storage to replace raw card numbers. This approach ensures that each subsequent charge pulls from verified tokens rather than exposed data, and it aligns with broader industry shifts toward automated monitoring tools that flag anomalies in real time.

Core Components of Merchant Account Verification

Verification processes typically unfold through several coordinated stages that begin with application review and extend into ongoing compliance audits. Banks and payment processors examine submitted documents including tax IDs, physical addresses, and financial statements, while they cross-reference these against public records to confirm operational authenticity. Data shows that this initial layer catches discrepancies early, such as mismatched banking details that could signal attempts to route funds through illegitimate channels.

Once approved, merchants integrate gateway tools that enforce additional checks during customer onboarding for recurring plans. Address Verification Service (AVS) matches billing information against issuer records, and Card Verification Value (CVV) confirms physical card possession at setup. These elements combine with 3D Secure protocols that prompt one-time authentication codes for high-risk profiles, and experts have observed that such layered defenses prove particularly effective in subscription services where charge patterns repeat monthly or annually.

Adaptations for Recurring Credit Card Flows

Recurring transactions demand verification methods that extend beyond one-time purchases because authorization must persist across multiple cycles without repeated customer input. Processors implement standing authorizations that reference initial verification data, yet they incorporate velocity checks and behavioral analytics to detect deviations like sudden geographic shifts or amount changes. According to reports from the European Central Bank, enhanced monitoring frameworks introduced around 2025 have helped standardize these practices across payment networks, resulting in measurable declines in unauthorized recurring activity by mid-2026.

Tokenization plays a central role here by substituting sensitive card information with unique identifiers that merchants never access directly. This separation limits exposure during storage and transmission, while dynamic verification updates occur through issuer communications that validate token usability before each billing run. People who manage subscription platforms often discover that these mechanisms integrate seamlessly with existing CRM systems, allowing automated retries on soft declines without triggering full re-verification unless risk thresholds activate.

Technological Safeguards and Monitoring Practices

Modern verification ecosystems rely on machine learning models that analyze transaction histories and flag patterns consistent with account takeover attempts. These systems review factors including device fingerprints, IP consistency, and purchase frequency, then they adjust authorization rules dynamically based on accumulated risk scores. Studies from the Bank of Canada highlight how such adaptive tools have strengthened recurring payment security in North American markets, where subscription growth continues to accelerate into 2026.

Merchants also navigate regulatory expectations that require documented verification trails for audit purposes. Compliance frameworks demand retention of authorization records and evidence of customer consent at setup, which helps resolve disputes when unauthorized activity surfaces later. This documentation becomes critical because it demonstrates adherence to rules that distinguish legitimate recurring flows from fraudulent ones, and it supports quicker resolution through chargeback processes when needed.

Implementation Considerations Across Industries

Industries such as software-as-a-service, media streaming, and utility billing apply these verifications differently yet follow shared principles that prioritize upfront validation. For instance, one study revealed that platforms incorporating multi-factor verification at subscription signup experienced lower rates of disputed recurring charges compared to those relying solely on basic card checks. Observers note that geographic variations influence implementation details, with regions emphasizing different combinations of biometric confirmation or real-time issuer queries to match local fraud profiles.

Collaboration between merchants, processors, and card networks further refines these protections through shared intelligence on emerging threat vectors. Updates disseminated in May 2026 emphasized expanded use of risk-based authentication for recurring authorizations, encouraging adoption of tools that balance security with minimal customer friction during billing events. This evolution reflects ongoing efforts to maintain trust in automated payment systems while addressing sophisticated unauthorized activity that targets stored credentials.

Conclusion

Merchant account verifications establish essential barriers that protect recurring credit card flows by confirming legitimacy at multiple touchpoints throughout the transaction lifecycle. Through combined document reviews, tokenization standards, and continuous monitoring, these processes create resilient frameworks that limit unauthorized access while supporting smooth subscription operations. Data from regulatory bodies across regions continues to guide refinements, ensuring that verification methods evolve alongside payment technologies and emerging risks into the latter half of the decade.