15 May 2026

Coordinating Support Networks with API Tools to Fortify Secure Credit Card Flows in Merchant Operations

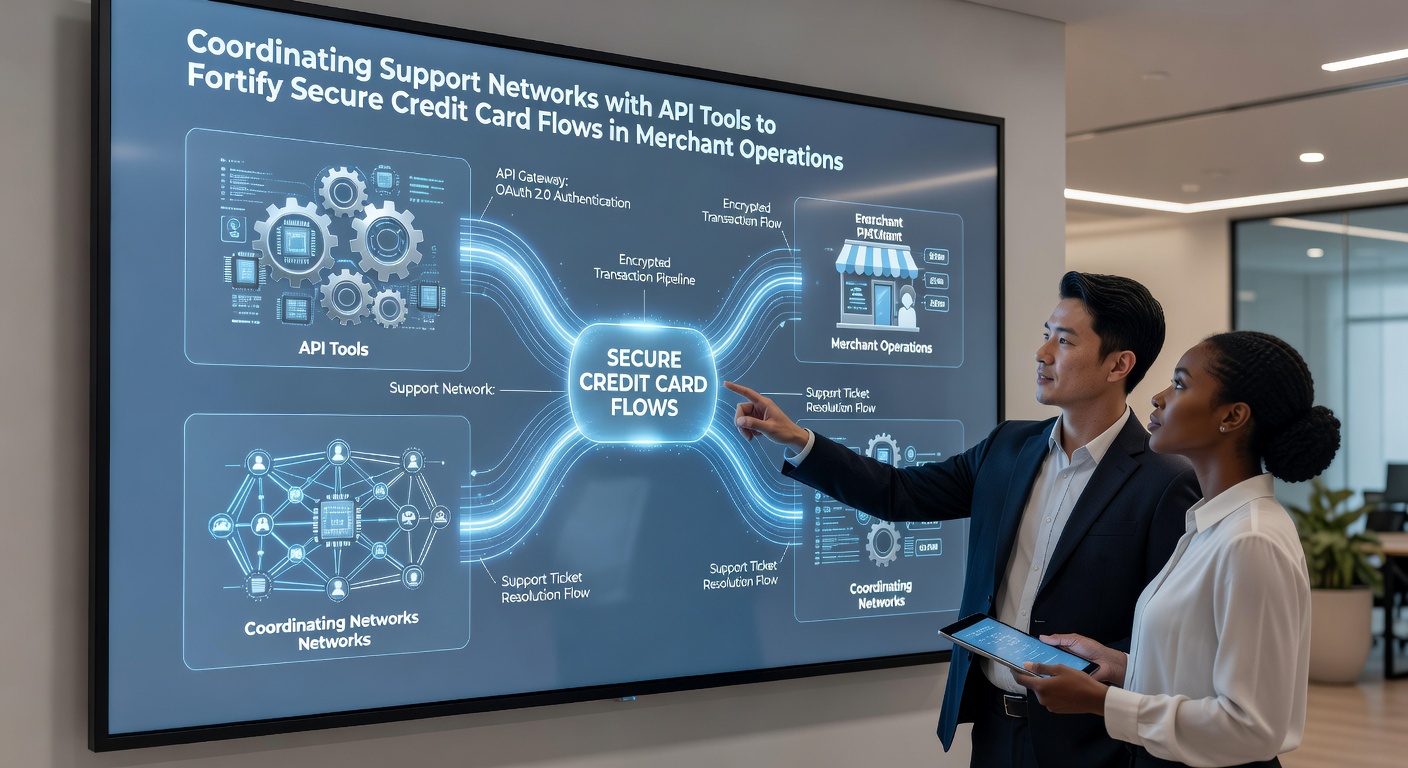

Merchants face mounting pressure to maintain seamless credit card processing while addressing real-time security demands, and coordinating support networks through API tools has become central to that effort. These integrations connect customer service teams, fraud analysts, payment processors, and issuing banks into unified systems that flag issues before they escalate. Data from the Federal Reserve's 2025 payments report shows transaction volumes climbed steadily through early 2026, with API-driven monitoring reducing unauthorized attempts across major networks.

Core Components of API-Driven Coordination

Support networks rely on standardized endpoints that pull transaction data, customer histories, and risk signals into a single dashboard. Developers configure these connections to trigger alerts when patterns deviate from established baselines, allowing teams to review flagged activity without pausing legitimate sales. Observers note that systems built this way handle thousands of concurrent requests while maintaining low latency, a requirement for high-volume merchants operating across multiple time zones.

Encryption layers sit beneath every call, and tokenization replaces card numbers with unique identifiers that limit exposure if any single point suffers compromise. Research indicates that merchants adopting layered API protocols saw measurable drops in successful fraud attempts by the start of May 2026, particularly in sectors handling recurring or high-ticket purchases.

Integration Patterns Used by Modern Merchants

One common architecture routes all authorization requests through a central gateway that simultaneously queries support databases for prior disputes or chargeback history. When risk thresholds are crossed, the system pauses the flow and routes the case to human reviewers who can approve, decline, or request additional verification. This approach keeps average response times under three seconds, preserving conversion rates while tightening controls.

Another pattern incorporates machine-learning models trained on anonymized transaction sets. These models update weekly and feed scores back through dedicated API channels so support staff receive prioritized queues. Figures reveal that organizations using this method resolved over 85 percent of flagged cases within the first hour during the first quarter of 2026.

Security Protocols and Compliance Requirements

PCI DSS standards mandate that any API handling cardholder data must segment networks and enforce strict access controls. Merchants achieve compliance by routing sensitive fields through isolated microservices that never store raw information beyond the transaction window. Auditors check these flows regularly, and systems that fail segmentation tests face immediate remediation requirements.

Token vaults managed by third-party providers further reduce the merchant's attack surface. Each vault issues temporary credentials that expire after a set period, and revocation happens instantly if suspicious activity appears. The European Central Bank published updated guidelines in late 2025 that encourage similar tokenization practices for cross-border flows, and many platforms aligned their APIs with those recommendations ahead of May 2026 deadlines.

Case Examples from Different Sectors

Retail chains processing high volumes of in-store and online sales have deployed unified APIs that link point-of-sale terminals directly to back-office support systems. When a card declines at the register, the same record appears in the merchant's dispute portal within seconds, allowing staff to contact the customer before they leave the premises. This coordination cut repeat declines by noticeable margins during holiday periods.

Subscription services face different challenges because failed payments can trigger cascading account issues. Their API setups monitor retry logic across multiple processors and escalate persistent failures to retention teams who can offer alternative payment methods. Records show such integrations preserved recurring revenue streams more effectively than manual follow-up processes used previously.

Challenges in Scaling These Systems

Legacy point-of-sale hardware sometimes lacks native API support, forcing merchants to insert middleware layers that add complexity. Teams must also manage rate limits imposed by card networks to avoid throttling during peak traffic. Observers note that careful load balancing and asynchronous queuing solve most bottlenecks, yet initial setup still requires specialized engineering resources.

Data privacy regulations add another constraint. Merchants operating in multiple jurisdictions must map which fields can cross borders and which must remain localized. API gateways with region-aware routing help enforce these rules automatically, reducing the chance of accidental non-compliance.

Future Developments Expected by Mid-2026

Industry working groups continue refining open standards for support-to-payment APIs, aiming for plug-and-play compatibility across providers. Early adopters testing these specifications report faster onboarding of new processors and quicker rollout of fraud-detection modules. The trajectory points toward greater automation where routine verifications happen without human intervention, freeing support staff for complex cases that still require judgment.

Conclusion

Coordinating support networks through well-designed API tools strengthens the security posture of credit card operations without sacrificing speed or customer experience. Merchants who implement these connections gain visibility across every stage of the transaction lifecycle, enabling faster responses to emerging threats. Continued alignment with evolving standards will determine how effectively these systems scale as payment volumes grow through the remainder of 2026 and beyond.